During the upcoming trading week, the economic calendar is heavily dominated by the United States, as the world’s largest economy releases inflation, retail sales, and consumer sentiment data.

Other key highlights on the economic docket this week include the release of United Kingdom jobs data, at a time when the Bank of England is warning that the nations growth prospects are starting to flatten.

This week will also see the release of monthly jobs data from Australia economy, a key speaks from Reserve Bank of Australia Governor Lowe, and CPI inflation data from the Canadian economy.

Something else to watch is sentiment. US and global stock market look frothy at current level, as the growth prospects of the US and China worsen stocks could take a big hit.

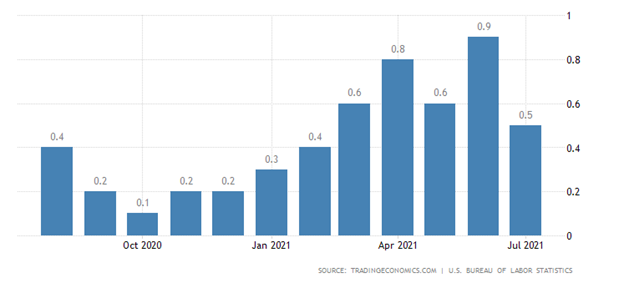

US CPI Inflation

The Consumer Price Index for the month of August is expected to show that inflation rose at a moderate 0.3 percent last month, which would be welcomed change from recent high CPI readings.

Last month US CPI increased 0.5 percent in July on a seasonally adjusted basis after rising 0.9 percent in June, the U.S. Bureau of Labour Statistics reported today. Over the last 12 months, all items index increased 5.4 percent before seasonal adjustment.

The closely watched food index increased 0.7 percent in July as five of the major grocery store food group indexes rose, and the food away from home index increased 0.8 percent. The energy index rose 1.6 percent in July, while the gasoline index increased 2.4 percent and other energy component indexes also rose.

{kind=link}