During the upcoming trading week the Jackson Hole Economic Symposium in Wyoming is set to headline the economic docket as traders await the latest thoughts from global central banks and answer the big question which is whether will change its dovish policy stance or not.

Other key macroeconomic releases to watch out for this week to watch include the release of the German IFO and Q2 reading, and also preliminary eurozone manufacturing PMI readings.

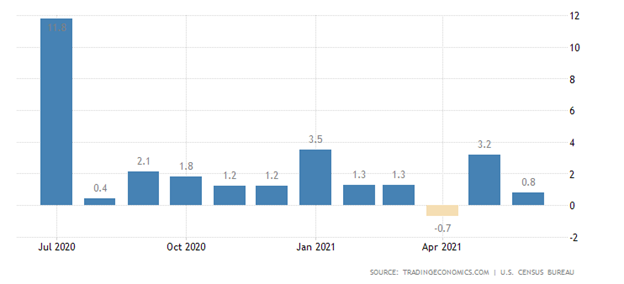

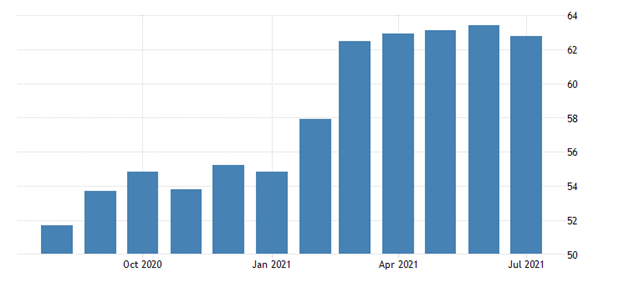

This week will also see the release of a raft of important data points from the United States prior to Jackson Hole, which include jobs, GDP, manufacturing, and durable goods orders.

Jackson Hole Economic Symposium

The highlight on the economic docket this week without a doubt is going to be the Jackson Hole event, which promises to be one of the biggest market movers for financial markets this year.

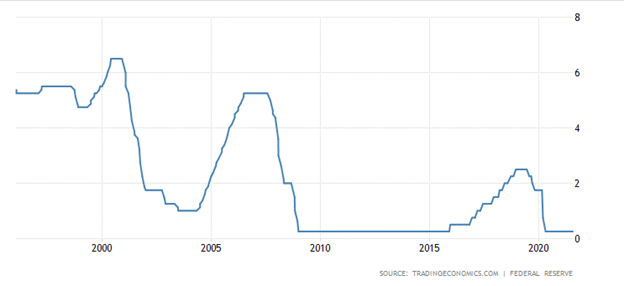

Expectations are ridiculously high that the FED will outline a date for tapering, following last week’s FOMC meeting minutes which seemed to suggest that FED members gave a large nod towards QE tapering. News that the meeting is being held virtually has somewhat pushed back expectations.

During the last policy meeting in July Fed officials expressed a range of views on the appropriate pace of tapering asset purchases, but most noted that it could be appropriate to start reducing the pace of asset purchases this year, provided that the economy was to evolve broadly as they anticipated.

{kind=link}