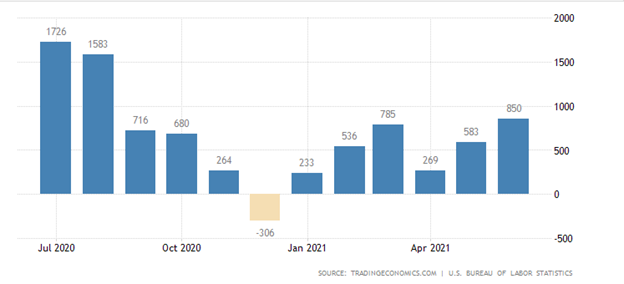

During the upcoming trading week, the release of the United States Non-farm payrolls job report is set to be the main focus for financial markets, following last month’s multi-month high 850,000 headline number.

Other key highlights on the economic docket this week include the closely watched ISM manufacturing report, UK PMI manufacturing report, and key retail sales numbers from the eurozone economy.

This week we also see a large emphasis being placed on central banks, with both the Bank of England and the Reserve Bank of Australia delivering monetary policy statement and interest rate decisions.

ISM Manufacturing Report

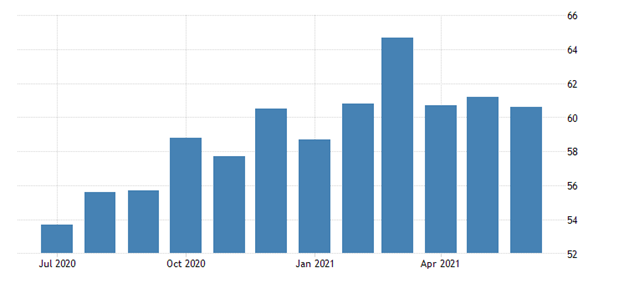

Analysts are expecting another weaker ISM manufacturing report for July, with a 60.5 number being touted as the most likely headline number this week. The ISM Manufacturing PMI fell back to 60.6 last month, which was some way away from highs of the year, as highlighted by the chart below.

If we look at last month’s reading, the data still pointed to robust growth in factory activity although a slowdown was seen for new orders, and supplier deliveries, while employment contracted slightly, and price pressures intensifies.

This month the ISM survey is expected to show more record-long raw-material lead times, wide-scale shortages of critical basic materials, rising commodities prices and difficulties in transporting products.

{kind=link}