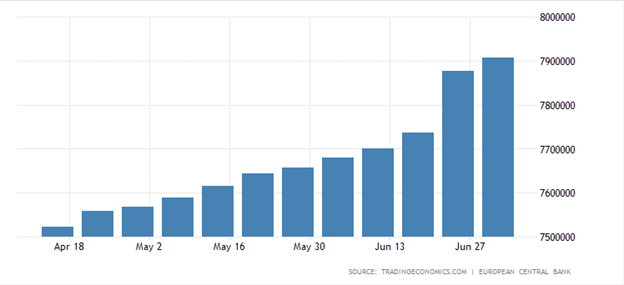

During the upcoming trading week the European Central Bank policy meeting is set to headline the economic docket as traders await the latest thoughts from the Governing Council on eurozone economic activity and whether the central bank is set to change its dovish policy stance.

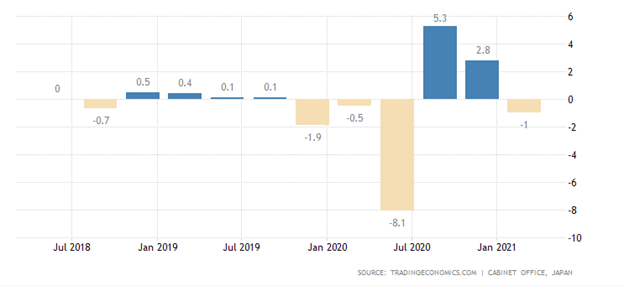

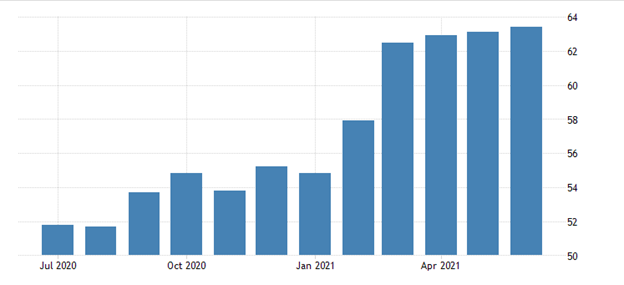

Other key macroeconomic releases to watch out for this week to watch include the release of the RBA and Bank of Japan meeting minutes and eurozone manufacturing PMI readings.

This week will also see the release of the People’s Bank of China interest rate decision and US earnings seasons as it starts to release second quarter earnings for tech, retail, and financial companies on the United States.

ECB Rate Decision

The highlight on the economic docket this week is without a doubt is going to the ECB policy decision, with inflation, growth, and progress on the central banks digital currency likely to feature heavily during the ECB press conference.

Last week the ECB announced that they are expected growth to pick up, so a more bullish stance is likely to be taken this meeting, however, the central bank is expected to stop well short of tapering QE.

{kind=link}