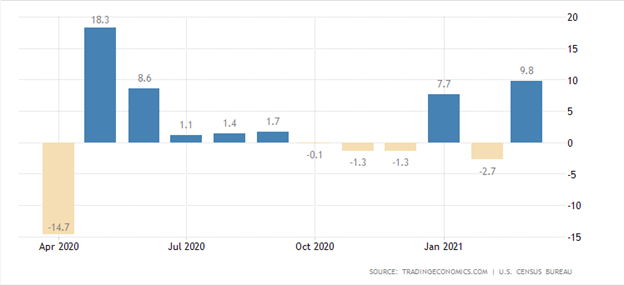

During the upcoming trading week, the release of the United States Consumer Price Inflation and Retail Sales data is set to be the main focus for financial market participants, as signs of inflation and increased consumer spending start to show up in the US economy.

Other key highlights on the economic docket this week include the Bank of England Governor Andrew Bailey holding a number of scheduled speeches after last week’s mildly dovish rate and monetary policy decision.

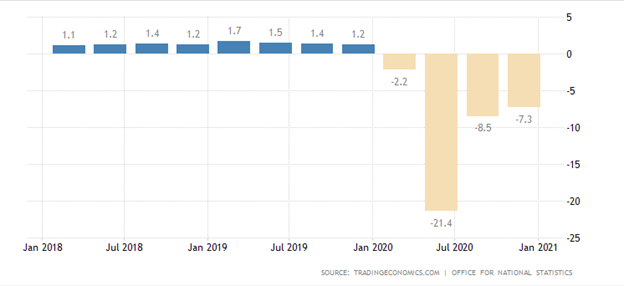

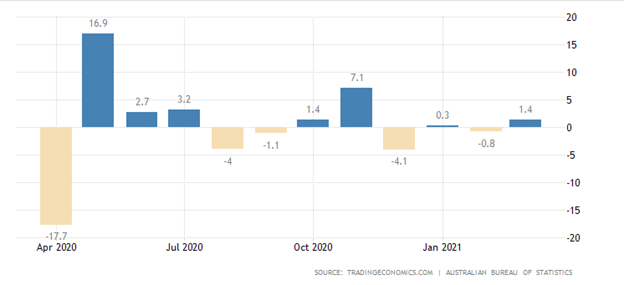

This week will also see Q1 GDP numbers from the United Kingdom economy, and monthly retail sales data from the Australian economy. Consumer confidence and weekly jobs data from the United States are also scheduled for release on the economic docket.

US Consumer Price Inflation & Retail Sales

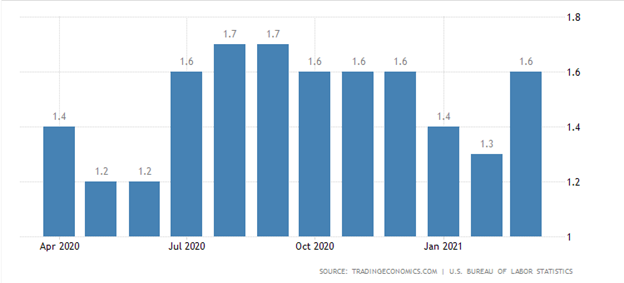

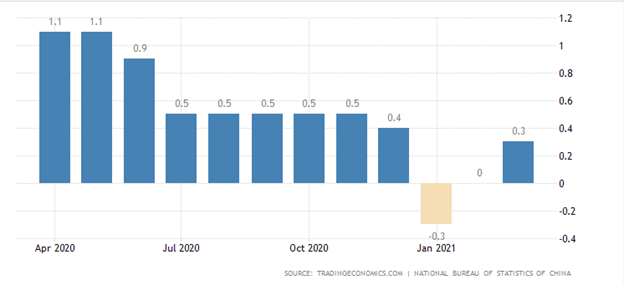

Traders will be braced for more volatility this week as US CPI inflation data is released, at a time when inflationary pressure is a hot topic amongst financial market participants. Current estimates suggest that month-on-month inflation is going to drop sharply against last month’s 0.6 percent rise.

Economists are predicting that CPI inflation will rise 0.2 percent while year-on-year inflation is set to rise by 2.3 percent. Things could be interesting if the annual CPI comes in on target, as year-on-year CPI inflation is set to break above the FED’s 2 percent target.