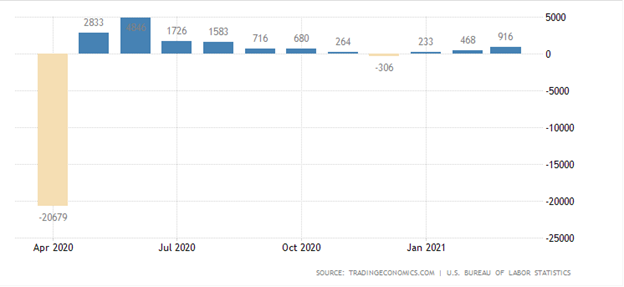

During the upcoming trading week, the release of the United States Non-farm payrolls job report is set to be the main focus for financial markets, following last month’s blockbuster 900,000 plus headline number.

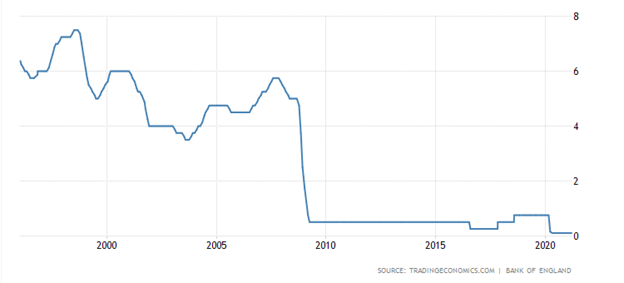

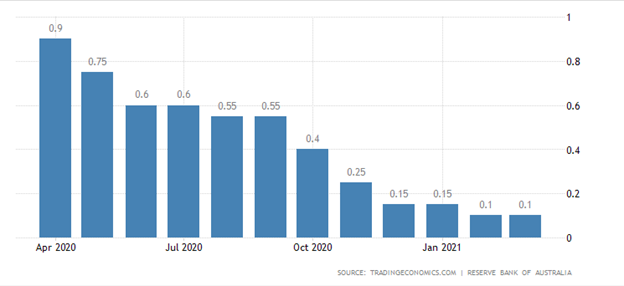

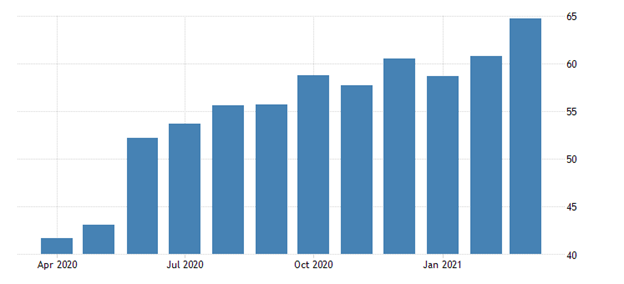

Other key highlights on the economic docket this week include the Bank of England and Reserve Bank of Australia interest rate decisions and monetary policy statements, and the ISM manufacturing report.

This week will also see retail sales numbers from eurozone and Germany, monthly jobs data from the Australian and New Zealand economies, and the Bank of Japan meeting minutes.

Non-farm Payrolls Job Report

Traders will be braced for another extremely strong Non-farm payrolls job report this week, with many analysts predicting that the United States economy created 925,000 new jobs in April.

Investors will also be on the lookout for any revisions to last month’s blockbuster 916,000 headline number. Additionally, the US Unemployment rate is predicted to have dropped to 5.8 percent, which is down from the 6.0 percent headline number recorded last month.

As the United States economy comes out of lockdown the American employment situation is only expected to improve. The market reaction is likely to be positive for stocks and the greenback if Friday’s job report comes in broadly in-line with the markets expectation.

{kind=link}