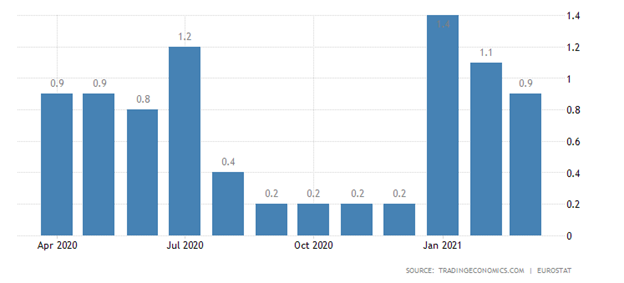

Last month the ECB increased the Pandemic Emergency Purchase Program, also known as PEPP. This was done to stop the eurozone economy slumping further, amidst a wave of fresh COVID-19 infection across the continent.

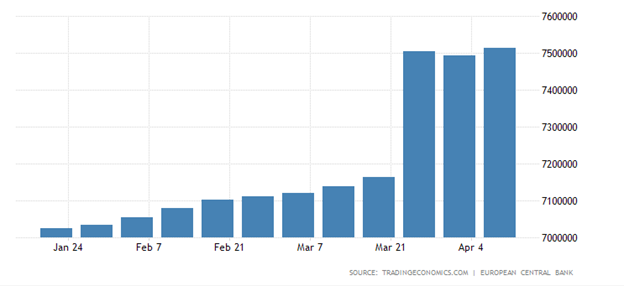

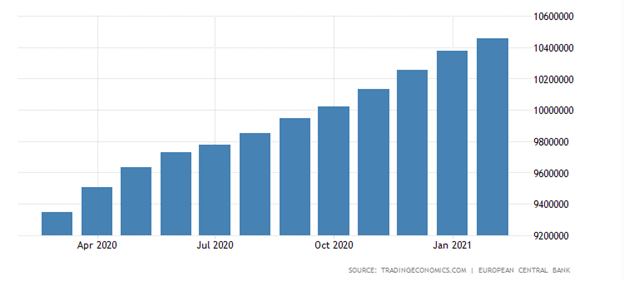

M1 money supply in the eurozone, which includes those monies that are very liquid such as cash, checkable deposits, money market funds, and traveler’s checks hit a new high after the PEPP program. M2 money, which supply is less liquid in nature, and M3, also skyrocketed.

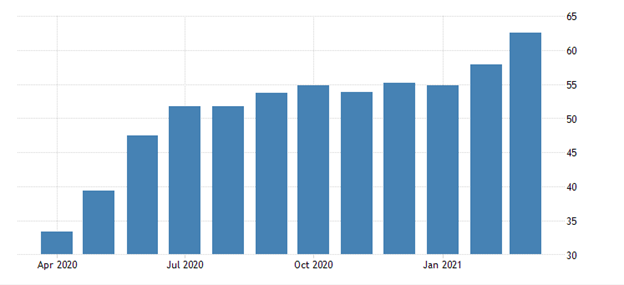

With so much money sloshing in the system it is hoped that the EU economy will keep trucking along until such time as the ECB can taper down QE as the continent comes out of lockdown.

The big risk for the ECB is a third COVID-19 lockdown, which risks further market distortions. One only must look at the volatility in the stock market, and indeed the crypto market to see where the money is being deployed, and re-deployed.

{kind=link}