Morning Brief

Market sentiment is attempting to improve in early-Wednesday trade as market participants digest the recent slowdown in Chinese economic data and the rise in COVID-19 cases globally, and of course the latest lockdown in New Zealand.

The US dollar index is holding firm after enjoying strong demand yesterday amidst safe haven buying demand. All eyes will be on the 93.20 to 93.40 price zone today and whether bulls can stage a breakout above that area or whether risk-on sentiment will cause the buck to sell-off again.

Gold is trading higher, which further hints that risk-off tones are still lingering, however, US 10-year yields are rising and already up 1.4 basis points. On the positive front S&P 500 futures and European futures are mildly positive and the Nikkei closed the day 0.9 percent higher.

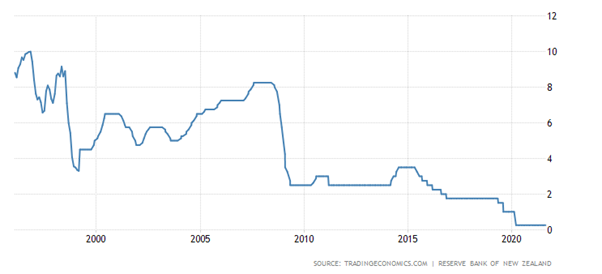

A very lively Asian session today doe to the Reserve Bank of New Zealand policy decision, which had been the subject of much-speculation this week due to the fact that investors were actually expecting a rate hike.