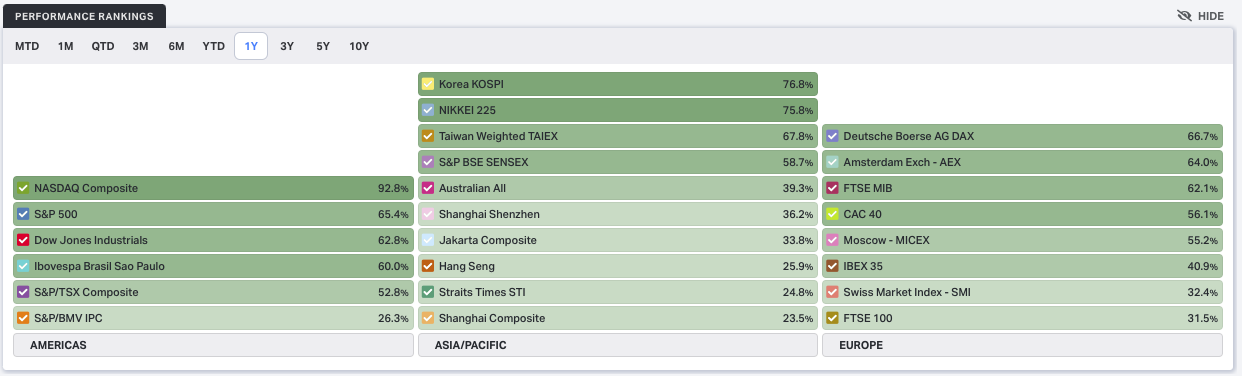

From April 2018 to the present day the majority of the world indices are positive, with only the IBEX35, FTSE100 and Hang Seng below the 0% growth watermark. At the opposite end of the spectrum, the Nasdaq100 is the clear winner at up 80% in comparison, of which most of the gains really happened in the last 365 days.

The FTSE and Hang Seng have both suffered under political uncertainty. With the UK in limbo for several years whilst we awaited the outcome of Brexit. For the Hang Seng, the political unrest that saw citizens demonstrating on the streets pre-covid has also signalled a flight from their index.

So today if we look at the biggest gainers of the pandemic flows our attention is focused on the Nasdaq, the Korean KOSPI, and the Nikkei 225, all up 95.6%, 76.8% and 75.8% respectively.

The Nasdaq has drifted down to the 13000 level ahead of the FOMC data release today and looks likely to hold around there from the start of the US session. However, it has been showing more signs of the volatility of late and for some retail traders, their eye is on a possible head and shoulders pattern. The price action from mid-January 2021 through to the present day has seen new all-time highs print forming the peak of the head in the H&S pattern, with the neckline spanning between the January and February 2021 lows. If this bearish reversal pattern were to play out the targets below are 11500 to 10200, depending on whether the measured move is 1 or 2 times the distance from the head to the neckline.

However, this could be a retail trader bear trap and we should look to reasons why the Nasdaq has not performed as well of late compared to say the Dow Jones Industrial Average or the S&P500.

The mega-bull run-up for the Nasdaq was based on the change in habits of the population who had to rely heavily on the technology companies that make up the composite index. The likes of Microsoft, Google, and Zoom competed for dominance over the software we all use now to conduct business. Netflix entertained us whilst we were locked in our houses for 23 hours a day and Amazon delivers all of our goods while the retail outlets remain closed for business during the lockdown. The vaccines that have come on-line in the last few months are having a marked difference in the populations that have been quick to administer them. With excess deaths and hospitalisations falling from the Christmas period highs. So we will be returning to work or going about our daily lives more outside of our homes and in our traditional places of work, making our reliance on these tech stocks a little less.

We have also seen the yield curves in the US Treasuries steepen and the relationship has been as the yields spike higher, the Nasdaq price action dips, and vice-versa. This suggests that the companies and especially the largest companies within the index are sensitive to inflationary expectations. So, if the Fed is correct and inflation is transitory, we should see the yields come down steadily, and therefore the signal as to whether the Nasdaq still has some new all-time highs to find should be evident on its performance when we observe yields falling again.

{kind=link}