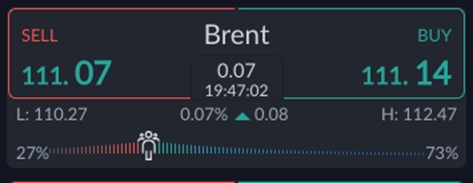

The Brent daily chart is now treading water within the range as the retail sentiment grows to an extreme level of bullishness. The general rule I follow is to fade extreme sentiment and to expect the market to break in the opposite direction of travel when leaving a trading channel.

The USA is a net exporter of oil and yet they have sent two senior officials of the Biden administration to Saudi Arabia to try and get a deal with the OPEC leader, Israel, and Egypt with regards to a possible oil production increase. President Biden will have a hard time of things in the mid-term elections if the voters don’t see a reduction in inflation, which is being driven higher by rocketing energy prices.

{kind=link}