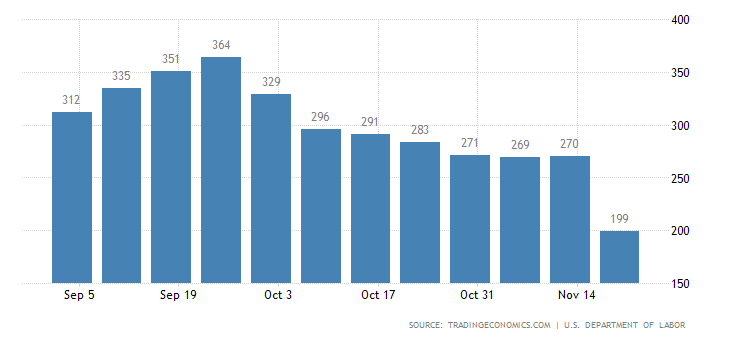

According to today’s US weekly jobless claims data, the number dropped to a 52-year low, which is great news for the FOMC, which are basically waiting for the jobs data to catch up with the inflation data. According to the US Department of Labour, initial jobless claims fell by 71,000 to 199,000 for the week ending November 20, the lowest level since November 15, 1969. This is the lowest point since March 14, 2020, and down by 21,000 over the last week’s revised average.

{kind=link}