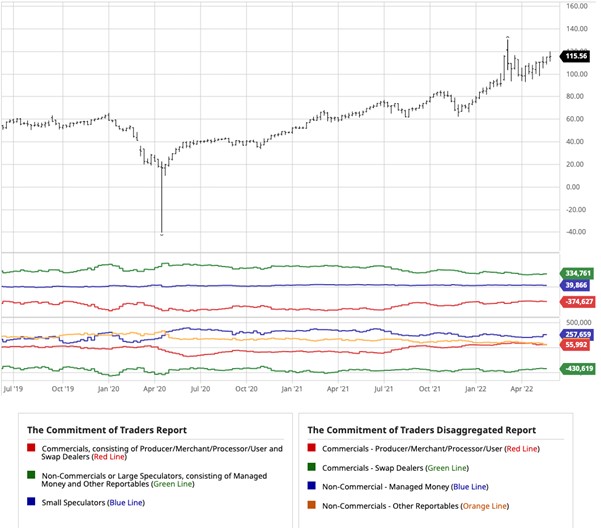

For refiners or producers of oil, the recent years have been good, and although the price of oil may be high, the amount of drilling and exports have helped the US at least, since they are net exporters and have received more cash for their product. In the Commitment of Traders report, we have started to see red lines edging down, which means that Commercials are adding to their short positions, which locks in these higher prices and puts more selling pressure on the market, which speculators who are long would be required to absorb to keep prices up. If the speculators decide to ease off, the price of crude will come lower, especially if the central banks cause a recession and destroy demand for commodities.

{kind=link}