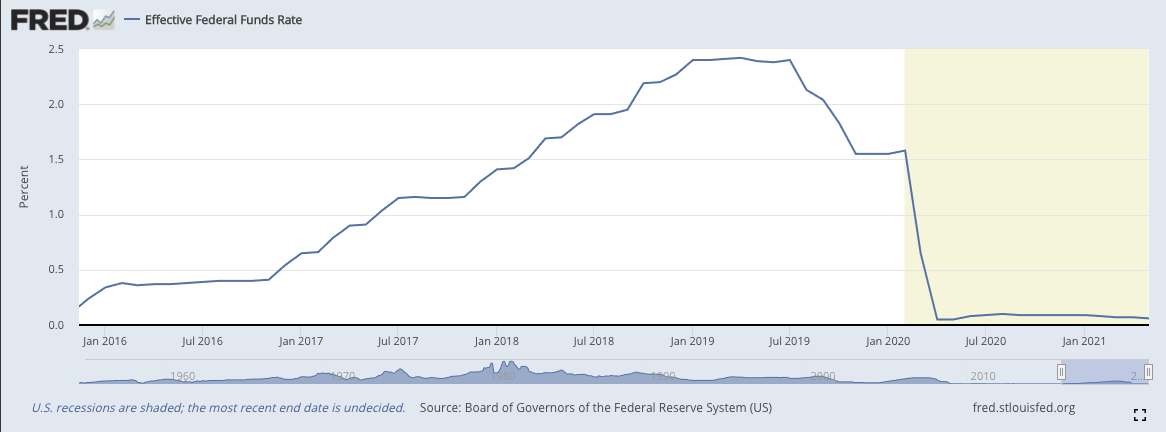

Before the FOMC last week, Treasury Secretary Janet Yellen expressed that she thought the Fed should raise interest rates and that it would be a good thing for the economy. As a former Federal Reserve Chair, she knows too well that during times of crisis the only thing the Fed can do to help is to lower the Federal Funds Rate (FFR) and to conduct Quantitative Easing asset purchases. The Fed does not want the FFR to go negative and with it being effectively at 0% there is no margin for error. Especially in a liquidity event or global economic downturn.

Last Wednesday the FOMC meeting gave the markets something to consider. A lot of market participants are working towards the Fed raising interest rates in the next couple of years to put a lid on the inflation that is seen currently in the Consumer Price Index (CPI). The Fed have said that they believe that the rising inflation as seen in the CPI is transitory and is in direct relation to the supply shocks that occurred when the global economy and supply chains broke down at the start of the coronavirus pandemic. Talk of reflation trade, infrastructure spending, global financial stimulus and re-openings of economies have weighed in on the inflation trade too, and the markets have until recently been convinced that this inflation story is going to run hotter because the Fed are willing to allow it to.

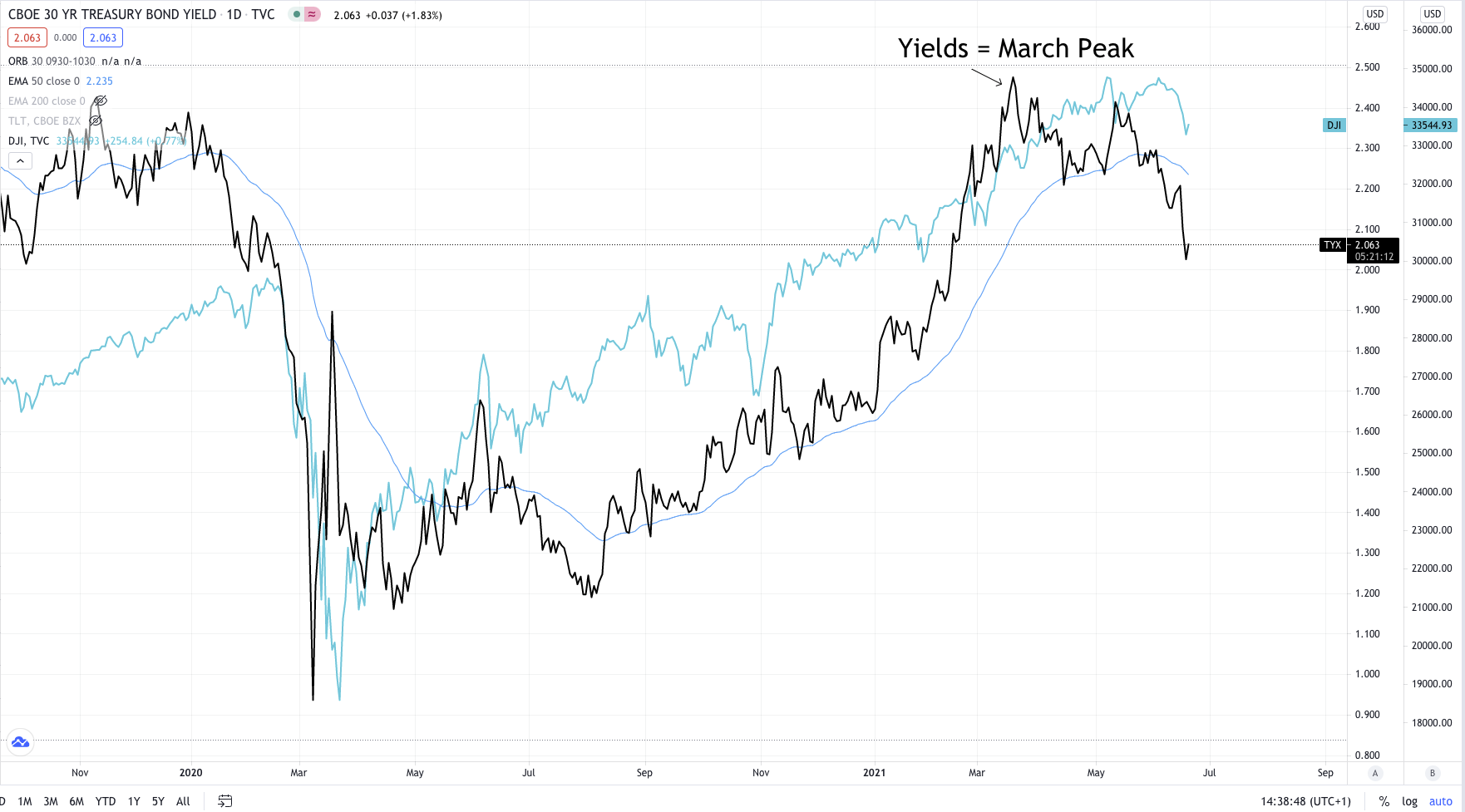

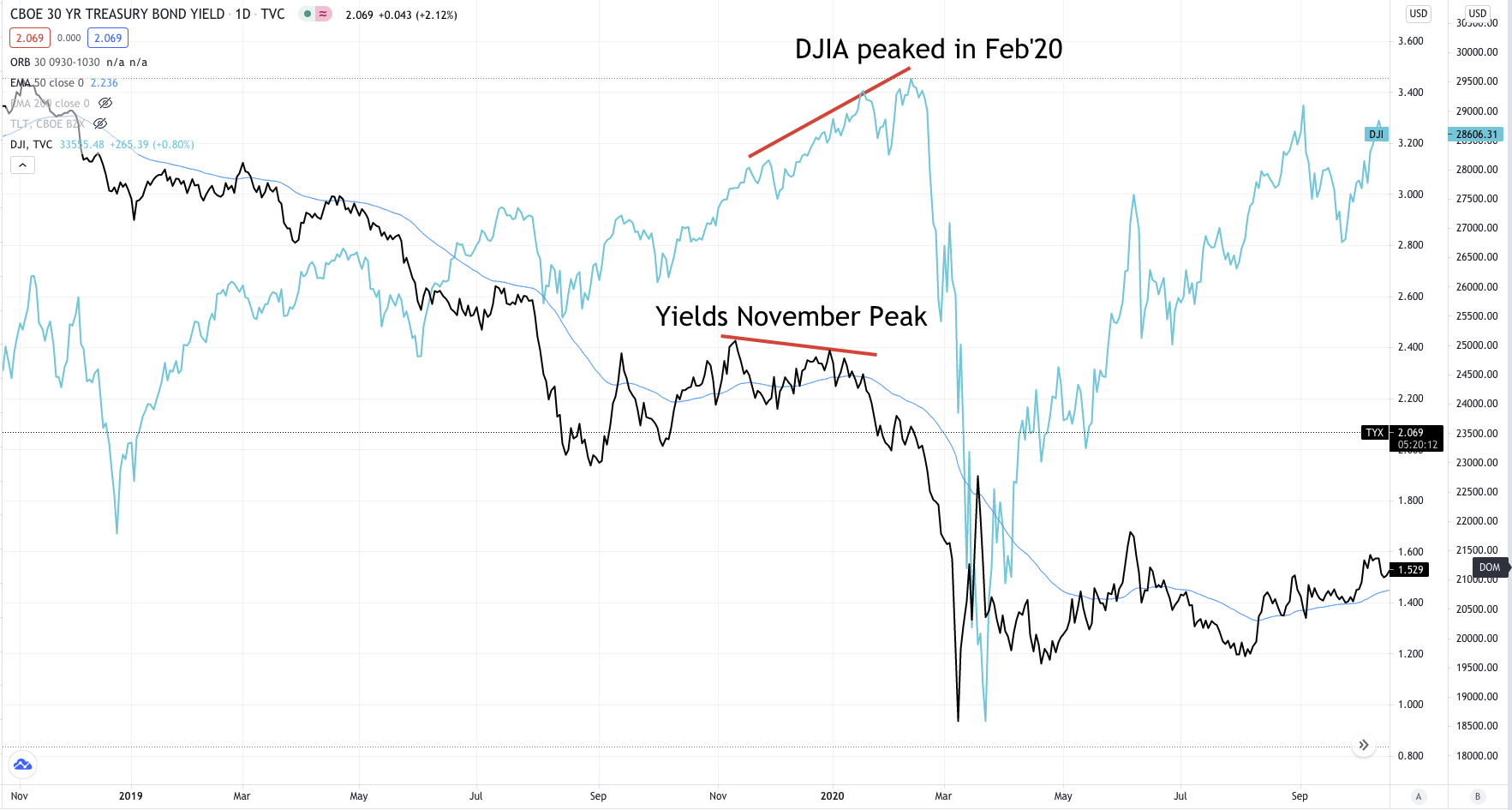

Yield curves steepening, commodity prices rising, cost of energy and food all add fuel to the inflation story fire. So why have the US bond yields stopped going up?

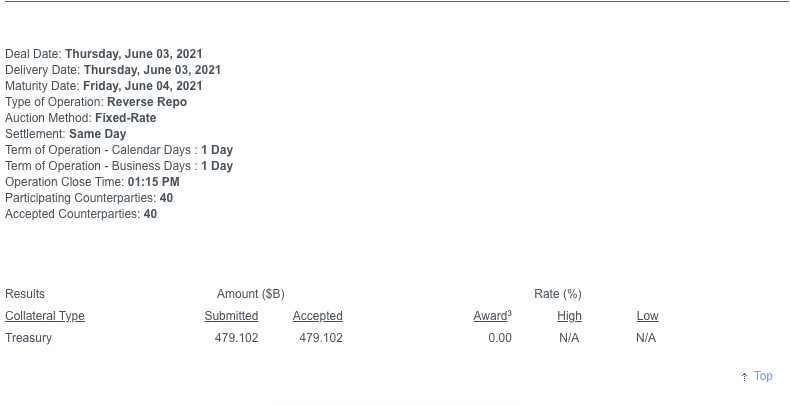

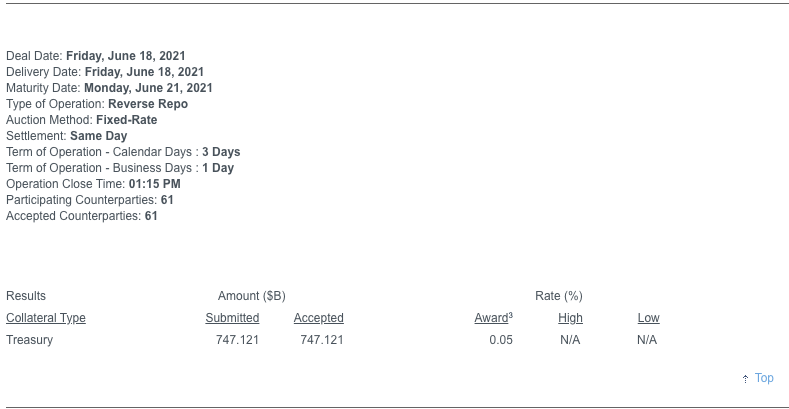

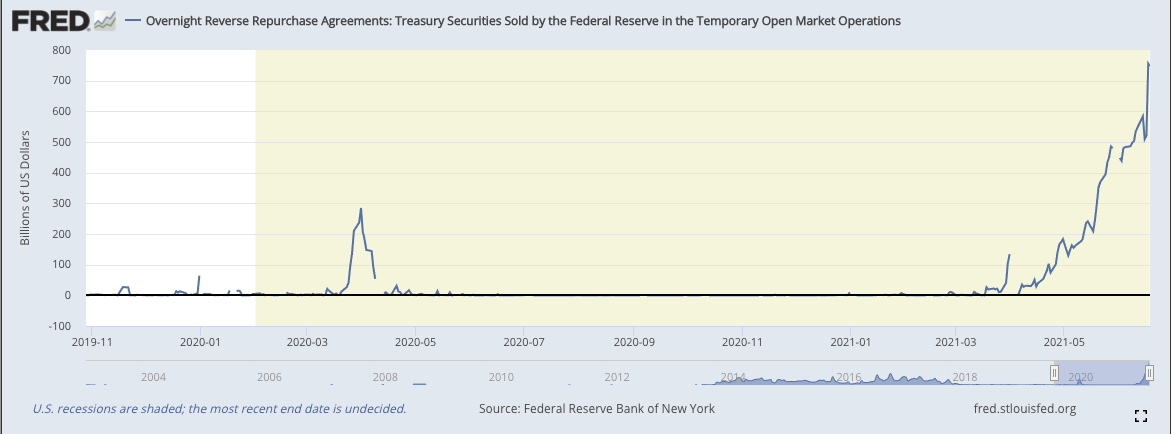

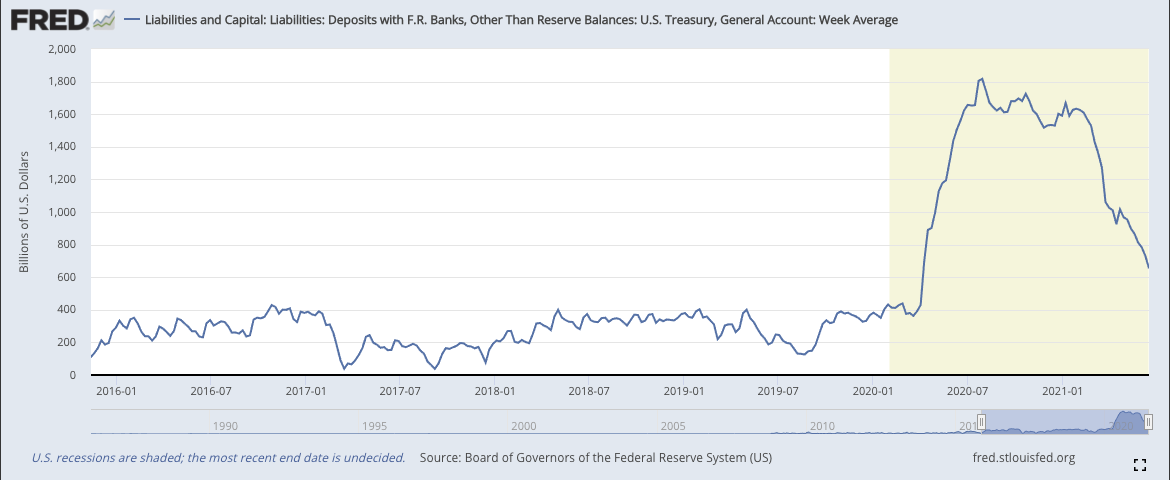

No monetary policy changes were made in relationship to the Feds dual mandate. The USA is still a long way off from full employment and the Fed who believe the price rises are transitory also believe that prices will stabilise once again when the base affects have all rolled out of the data. They did make a change to the interest on excess reserves (IOER) and added 5 basis points, or 0.05% to the interest rate paid to the overnight loan Reverse Repo program. So why would they have done that?

{kind=link}