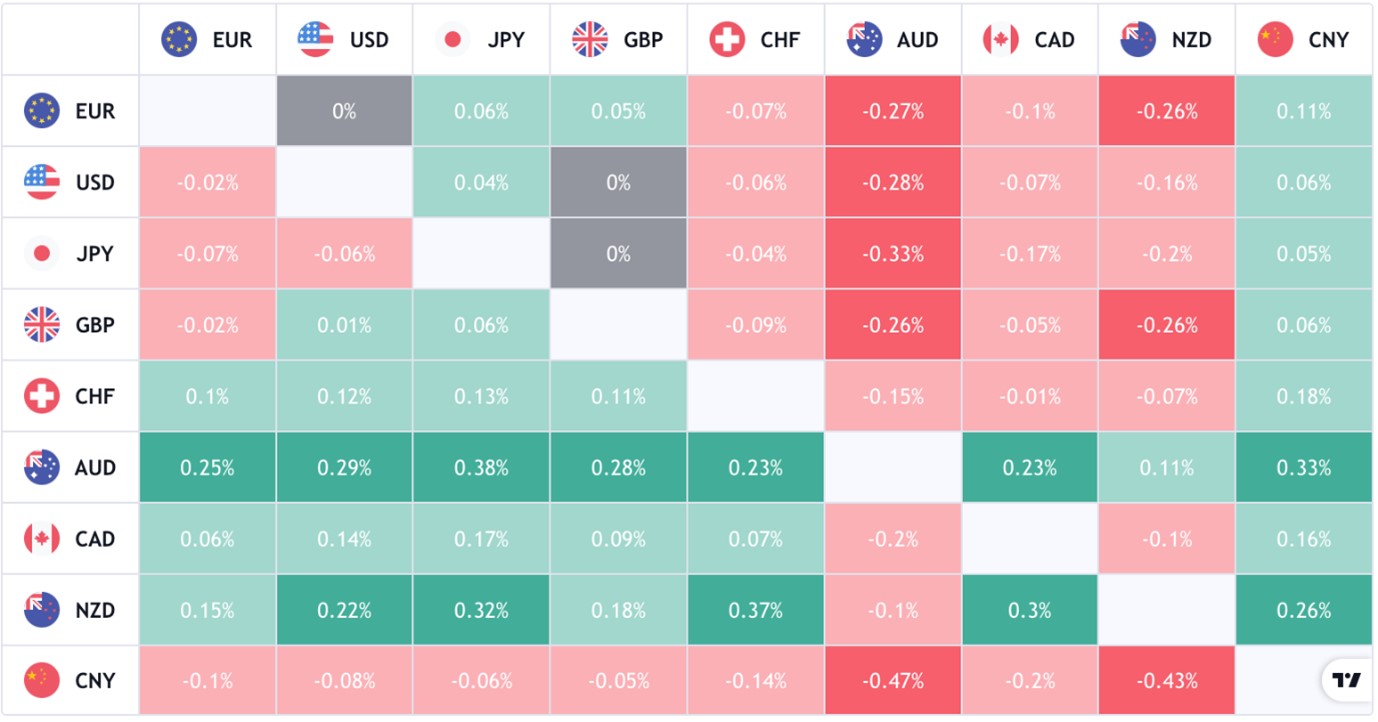

The AUDUSD has pushed higher towards 0.7300 with the next level of resistance at 0.7400. The AUDUSD is a good trending pair and after the retest of the descending trendline we could be going a lot higher.

Gazprom announced that gas transit via Ukraine continues, though it was noted that the Yamal-Europe pipe which had seen gas flow westwards to Germany is now stopped and flowing eastwards.

{kind=link}