Clearly the European Union will have to do something about the rising inflation that yesterday printed a record 8.1%. The price of energy now that the EU have begun to really move away from the Russian oil and gas could go higher on decreased available supply. The US may be pressured into returning to a ban on exports to get the voters on side during the mid-term elections. We just need to see if the producers see this as a cap in the rise and start hedging more aggressively, or whether they believe they can pump more and still command higher prices.

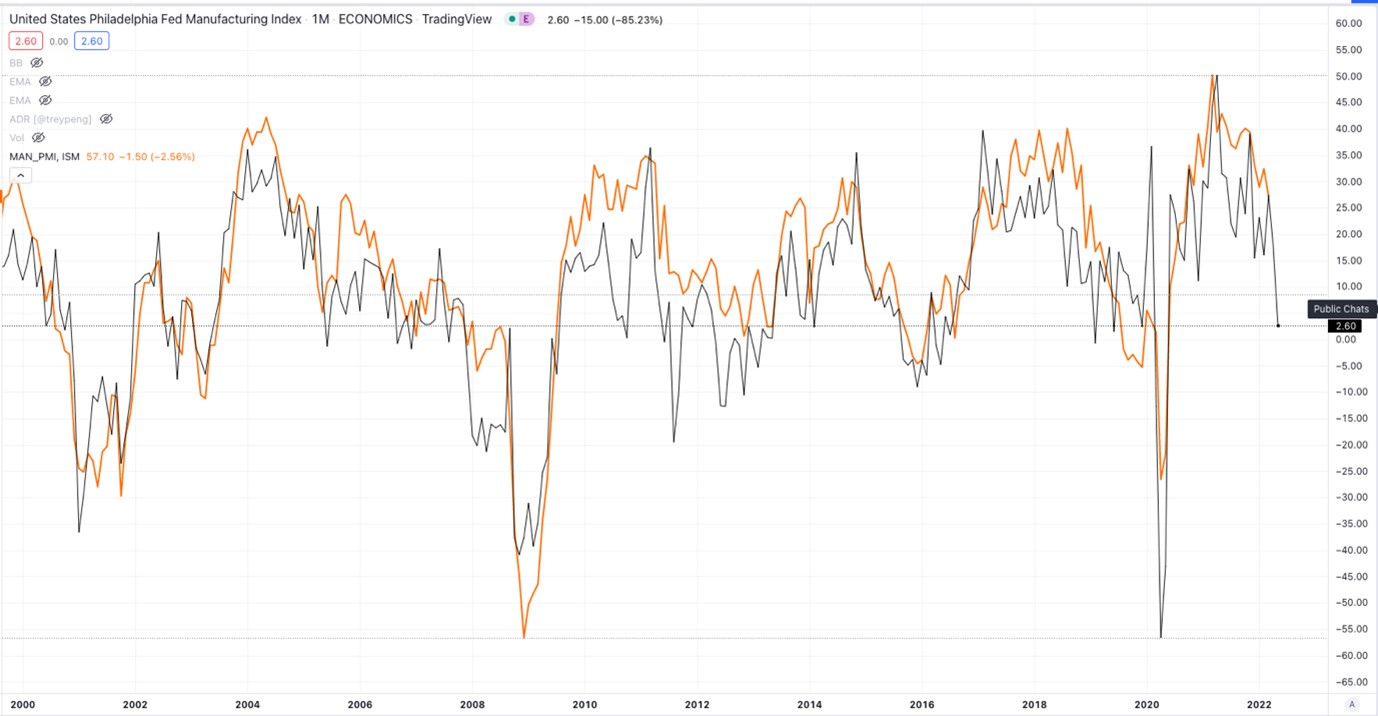

During the US session we have some market moving Tier-1 data, starting with the Bank of Canada rate decision, and then the US ISM Manufacturing PMI and JOLTS Job Openings. There then follows some key Fed speakers so we may have to wait until after they have concluded to see the true direction the market goes with tonight’s close signalling the moves for Thursday.

{kind=link}