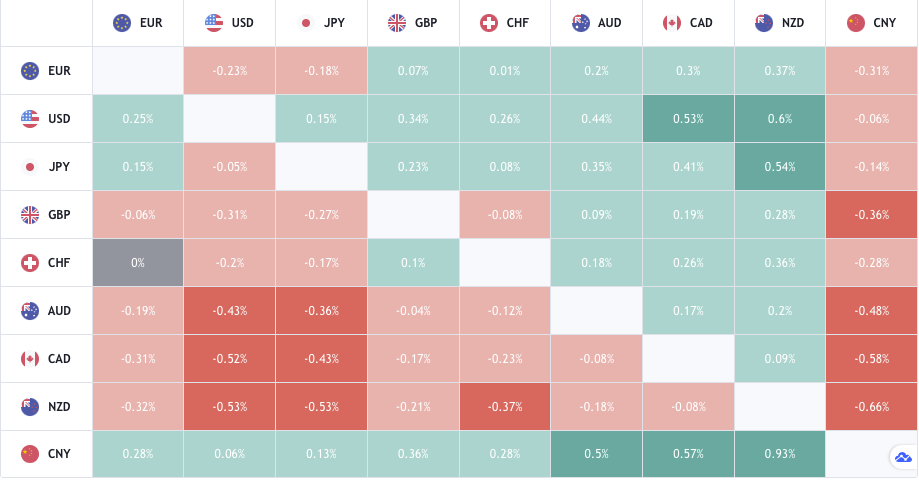

In today’s London session the forex markets have been trading against the US dollar strength. This week is a big week for the US dollar and USA’s economy, with CPI data out tomorrow and the semi-annual Fed testimony to congress. The Fed are very unlikely to react to the rising CPI as they have stated and will re-iterate this week that they are willing to allow the US economy to run hot for a longer period of time, that they are expecting inflation to last longer but ultimately, they see it as a transitory effect and that over the course of the year, the average inflation should be at or around their base case and within their target range.

The Reserve Bank of Australia are more likely to taper along with the likes of the RBNZ and BOC as those economies bar the COVID-19 disruptions are likely to have economies running hotter due to their close ties to the energy and metals markets.

{kind=link}