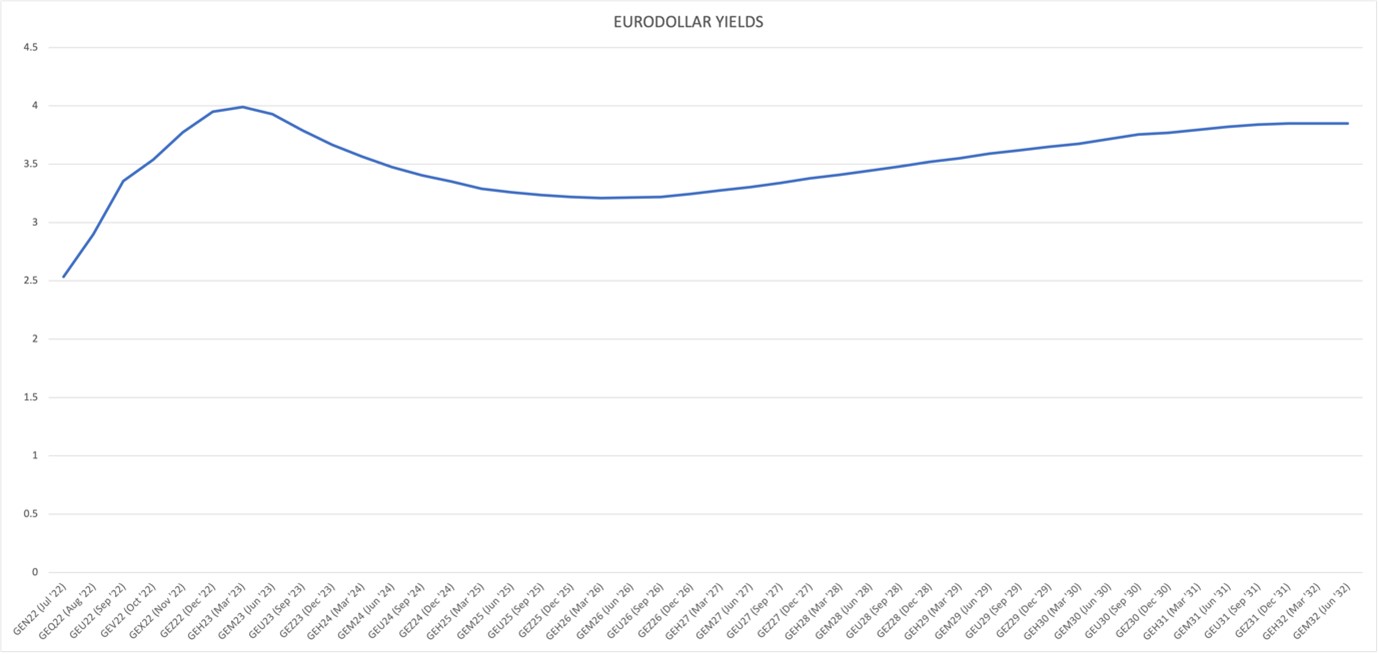

While last week’s 75bps hawkish policy update by the US Fed failed to move the US dollar higher, the Fed announced its summary of economic projections with expectations of tightening even more aggressively through the rest of this year. According to market participants, the Fed’s policy rate is anticipated to peak between 3.50% and 4.00% by mid-2023, after which the Fed will need to reverse course and begin cutting rates heading into 2024. The Eurodollar yields are a key indicator in the broader market outlook. A rising curve shows that the deepest, most liquid and sophisticated money market is optimistic of the future. An inversion like we see in the contracts that span from 2023 to 2026 highlight that all is not well and that this market expects some market turbulence soon.

The Fed is actively trying to kill demand as they have no control over the supply side of anything. In the press conference after the FOMC decision Fed Chair Powell said that the Fed are not actively trying to cause a recession. But I have a feeling the markets, and especially the Eurodollar market doesn’t believe him.

{kind=link}