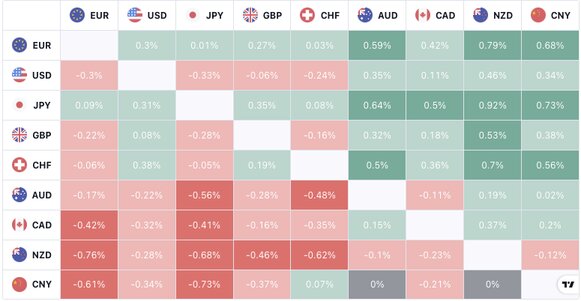

The pound is still relatively string against the US dollar despite the Brexit/N.I. uncertainty as GBPUSD trades around yesterday’s high and near the liquidity above 1.2630. This morning’s early UK data included UK government borrowing for April. This came in close to expectations and down from £23.4bn at the same point a year ago.

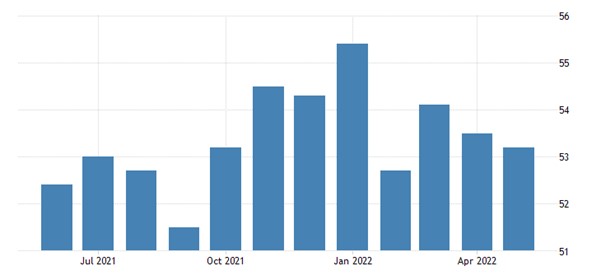

Yesterday we highlighted today as being all about new information that will come from the Flash PMI’s. We have European, UK and USA flash data today, so I am expecting some volatility at the data release. However, tomorrow the markets focus will be on the FOMC meeting minutes, so we must prepare for a spike and retrace in most major forex pairs today. The May readings will again be impacted by the Ukrainian crisis and by Covid restrictions in China but, overall, expectations are for some good numbers.

{kind=link}