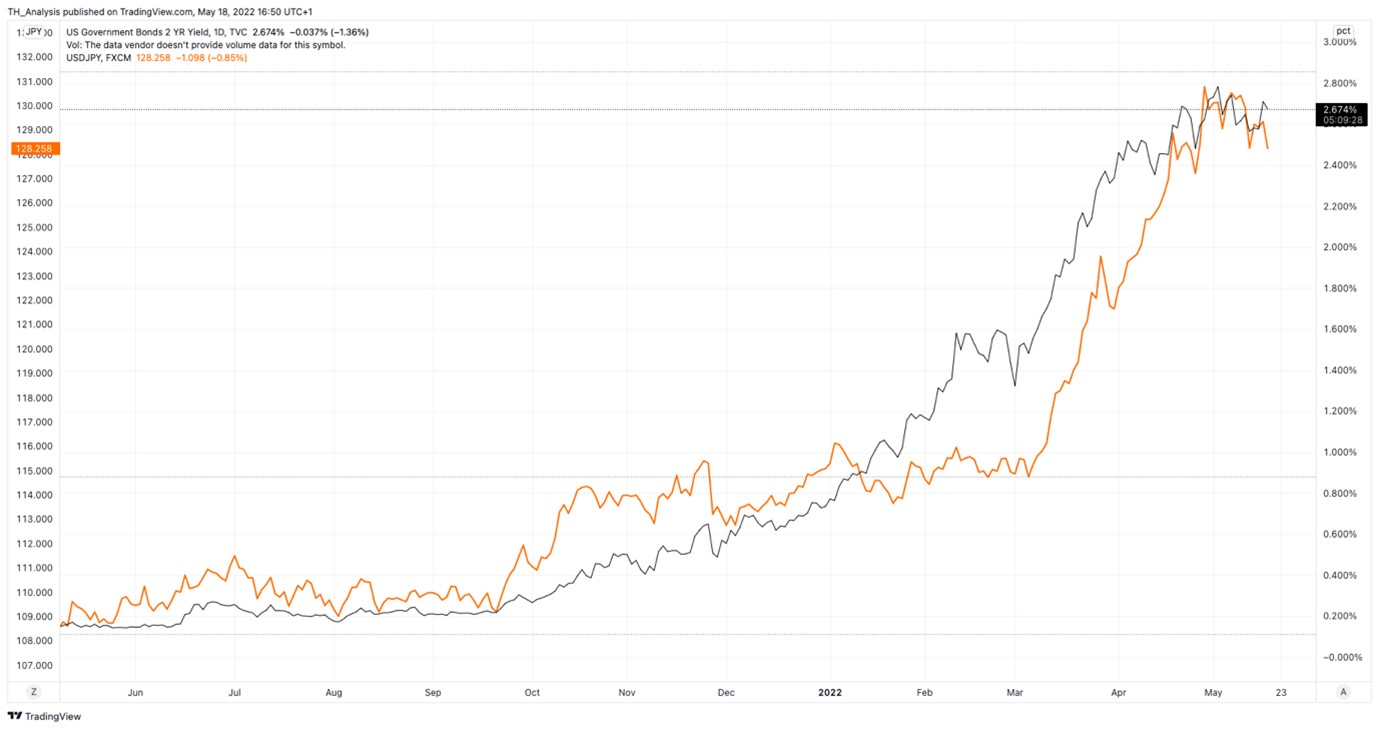

For quite a while the USDJPY was moving lower or higher with the US 2-year treasury yields. This is a relationship that can diverge when the yen is being pushed by other forces other than the divergence in central bank monetary policy. The relationship is one that is broken when the price of energy should change direction as the Japanese economy is predominantly based on exports of physical goods, which require fuel to distribute them. Today the strength in the Japanese yen across the major currency crosses has brought the USDJPY lower by -0.88% and this morning’s high UK CPI reading helped the GBPJPY to drop by 1.54% today. The formal request by Finland and Sweden to join NATO will add to the geopolitical nightmare brewing in Eastern Ukraine but could also have ramifications in the energy markets. Turkey is currently blocking them from joining NATO due to the two countries supporting the Kurds, which Turkey see as terrorists. When a country joins NATO, it usually ends up having a US military presence stationed there or can be used by the USA to launch manoeuvres from. This means that if the USA were to go to war with another country, all NATO members would be pulled into a war that they may not even agree with. Similarly, if Russia were to be aggressive with Finland, the USA would be on hand to help out, which is what President Biden reiterated today.

{kind=link}