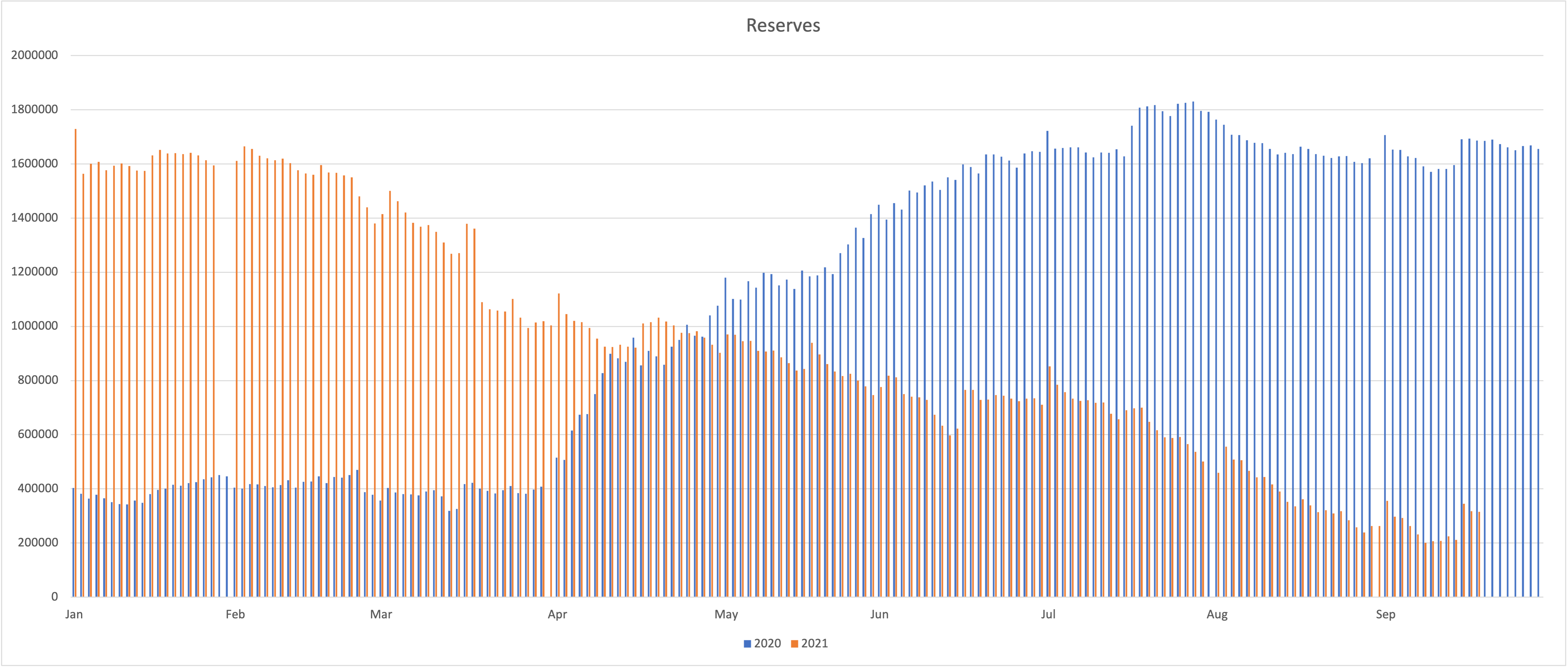

The above graphic is the build-up of the US Treasuries reserves (blue) held at the Fed during 2020 where they peaked at $1.8trln, which US Secretary Mnuchin had built up to pay for the COVID-19 extra expenses. The orange histogram shows how the current Treasury Secretary has had to draw down on the general account and get reserves back to a more normalised level.

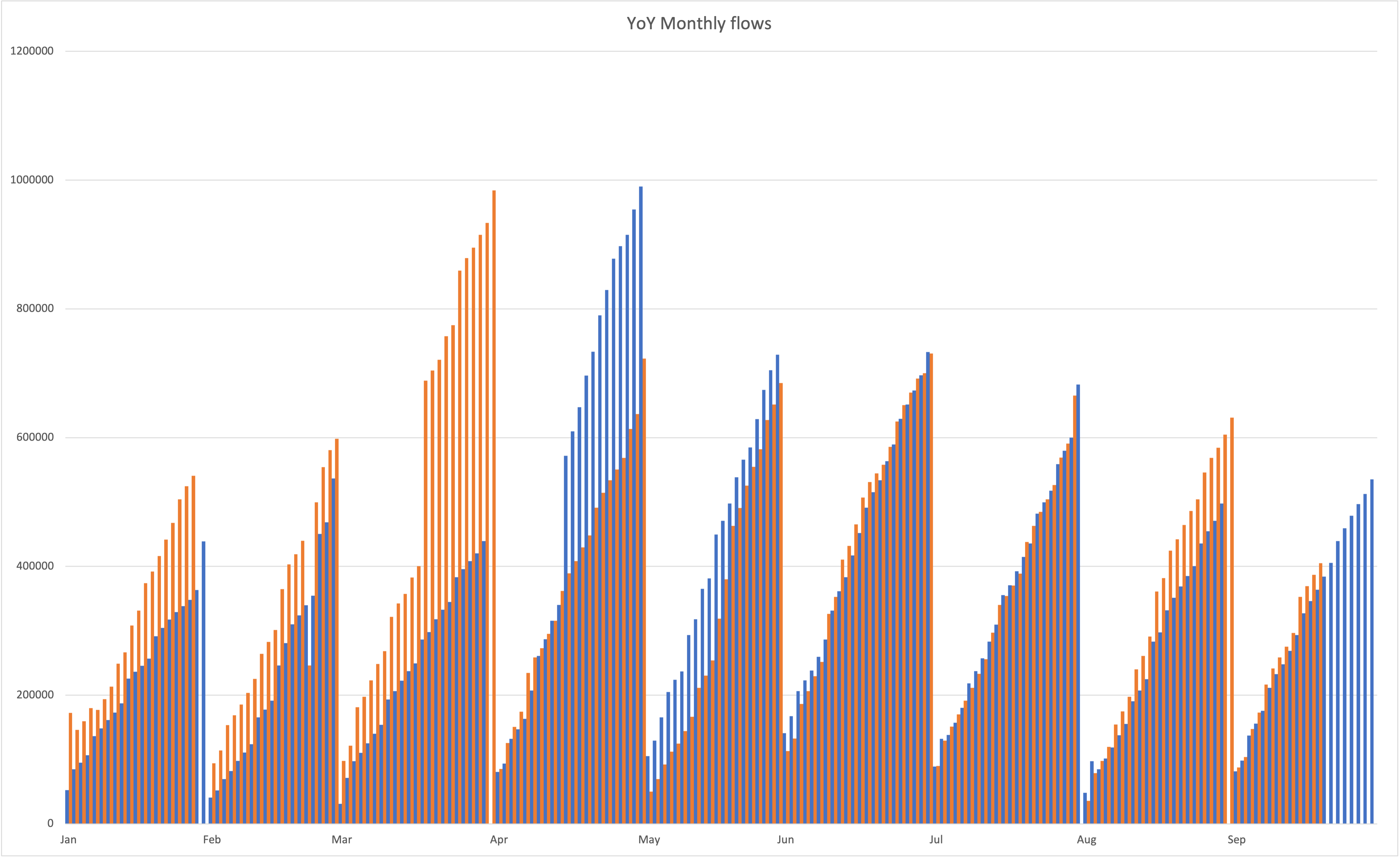

These reserves end up mainly on the commercial banks’ balance sheets and here lays reason that the NY Fed has doubled the RRP. The banks are receiving deposits at record levels and reserves which they need Tier-1 collateral to back. The highest form of collateral is the UST’s that the Fed is removing in their QE purchases. The Fed with the RRP swap back the cash held at the bank for the collateral held by the Fed in an overnight transaction, which means the banks meet the required levels of leverage set out in the Supplemental Leverage Ratio (SLR) regulations.

The SLR calculation is Tier1 capital / consolidated assets. Consolidated assets (the denominator) include Treasuries and reserves. The ratio must be 3% or greater. Most banks keep it well above 3% for stress test reasons. As the US treasury drained the TGA in 2021 the denominator in the SLR for the banks increased. Meaning the ratio gets smaller and potentially gets to the 3% threshold or even below. When that happens, the banks must either slow the rate of loan creation, sell liquid assets, or raise capital. The banks hold derivatives like stock options and futures, as well as assets, so it is highly probable that they sold some of their assets over the course of the last few trading days as buyers attempted to buy the dip in equities. Knowing the average retail trader was looking at the 50 ema as well as every asset manager on the planet, was probably too good a liquidity event to miss out on.

This type of market action hasn’t happened for a couple of years because the US debt ceiling was suspended. That all changed in August 2021 when the debt ceiling was reinstated, and the US Treasury was forced to stop selling new debt into the markets. When there wasn’t a debt ceiling to consider, the US Treasury would issue debt, which the banks would buy up, and in doing so this would drain the bank’s reserves and keep them within the SLR. In today’s FOMC press conference Fed Chair Powell said the US should never default on their obligations and liabilities as that would cause almost irreparable damage to the markets, and to an extent that the Fed may be helpless to control.

{kind=link}