Seeing a company go from riches to rags with a potential of a great comeback was too compelling for the retail traders who were coming to the Nokia stock on the back of GameStop. Since the peak of Nokia in the 2000 tech bubble, the share price had lost 90% of its value but anyone looking at the sloping trend line over the last 20 years will be seeing a potential for a real momentum change in the outlook of the stock, should the share price double from €3.94 to €8.

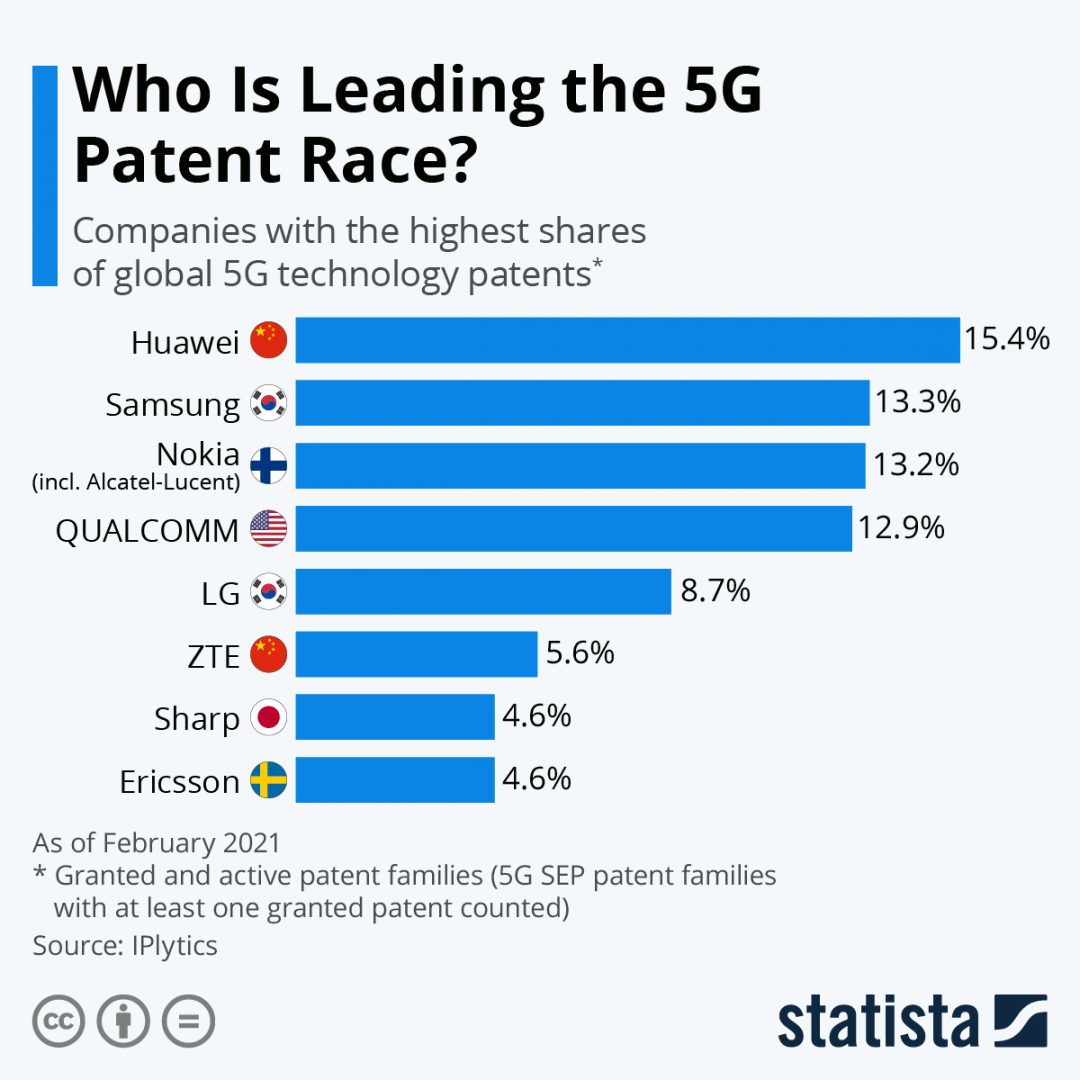

With the added interest in the tech space and the new 5G network being rolled out, it is interesting to see how the big players are jostling for the top position. Huawei with its dominance in patents is looking to start cashing in on the licensing deals, with every company using their technology having to pay royalties.

This tech world becomes very small and intertwined as companies have merged and choose to manufacture across the globe. China being the manufacturing centre for most companies, won the race to build the tech and have used this position to their advantage. Cloak and dagger nefarious dealings have occurred, and lawsuits have been filed with mobile phone/tech companies like Apple Inc. having a history of using Qualcomm chips from 2011, and Qualcomm having disputes with Huawei over intellectual property infringements. It is easy to see how certain key features are found across many devices.

A lot of this came to a head with the US administration effectively putting a stop to Huawei selling into the USA and imposing over $60billion in tariffs against China, it also added sanctions to countries willing to use Huawei for 5G infrastructure, which led the UK government to reverse course on their dealings with China on this matter.

It now turns out that Huawei is losing about 50% of its mobile phone revenue which is a good thing for Qualcomm who sees this gap in the market the way in which they will have exponential growth into 2022.

Qualcomm (QCOM)

Qualcomm is a technology company headquartered in San Diego, California. The company designs and creates software and chips for use in wireless equipment like mobile phones. Qualcomm also develops and commercializes wireless technologies and has previously licensed many technologies related to 3G and 4G technology.

As 5G gets rolled out, the IoT and connected devices will result in greater income for Qualcomm. In 2020, Qualcomm reached a new agreement with Apple for the supply of its chipset in a multi-year deal, and as 5G goes beyond mobile phones the IoT, immersive interactions, and Autonomous Vehicles, Qualcomm will remain not only well placed but a true leader in the 5G world.

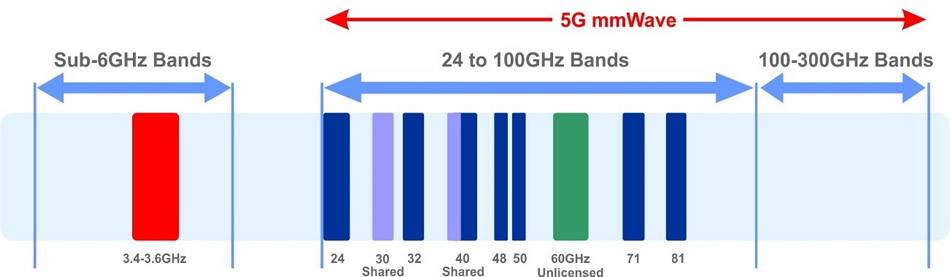

Since the 1990’s Qualcomm has been researching 5G, producing prototypes from 2016 following on from the 5G mmWave design in 2015.

{kind=link}