The world’s largest gold mining company is Barrick Gold, and they have their HQ in the USD, but China is the largest producer, with Russia and Australia coming in 2nd and 3rd place respectively.

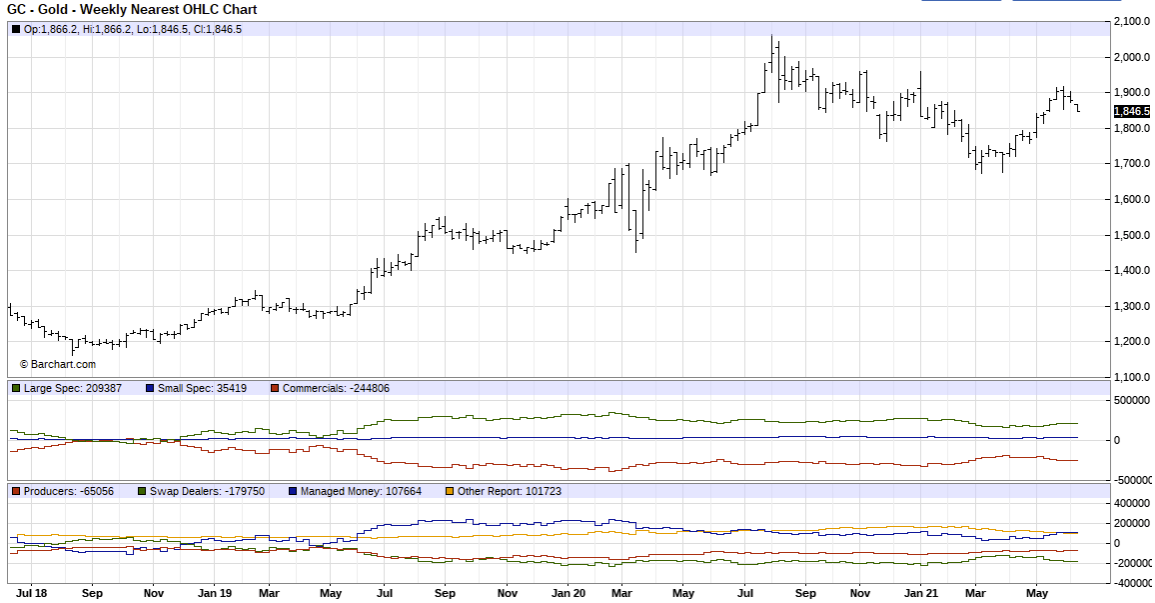

Investing in gold over the last 12 years may have been a bit of war of attrition with patience the key to long term riches. In 2008 at the height of the market crash around Lehman Brothers collapse gold found support at $700 and then pushed higher towards $1950. Quantitative Easing was supposed to bring in hyperinflation, but the hindsight analysis is that it did the opposite, and it took a while for economists to get their heads around why trillions of new fiat dollars were not creating the assumed Zimbabwe or Weimar Republic outcomes.

Currently gold has another narrative to deal with and that is the new supposed store of value that it has compared to the new kid on the block – cryptocurrency. Bitcoin has been put out there as being a new store of wealth, and one to replace physical gold as it is of limited supply and is easy to move around the world, with little cost in terms of delivering bitcoin or keeping bitcoin. Unlike gold which is hard to move around and has to be kept in a fortress at a high cost.

Gold miners though are benefitting from the renewed interest in the yellow metal and the prices that they see gold being sold for are much higher than the costs of production, so they are able to put more money into finding more resources.

{kind=link}