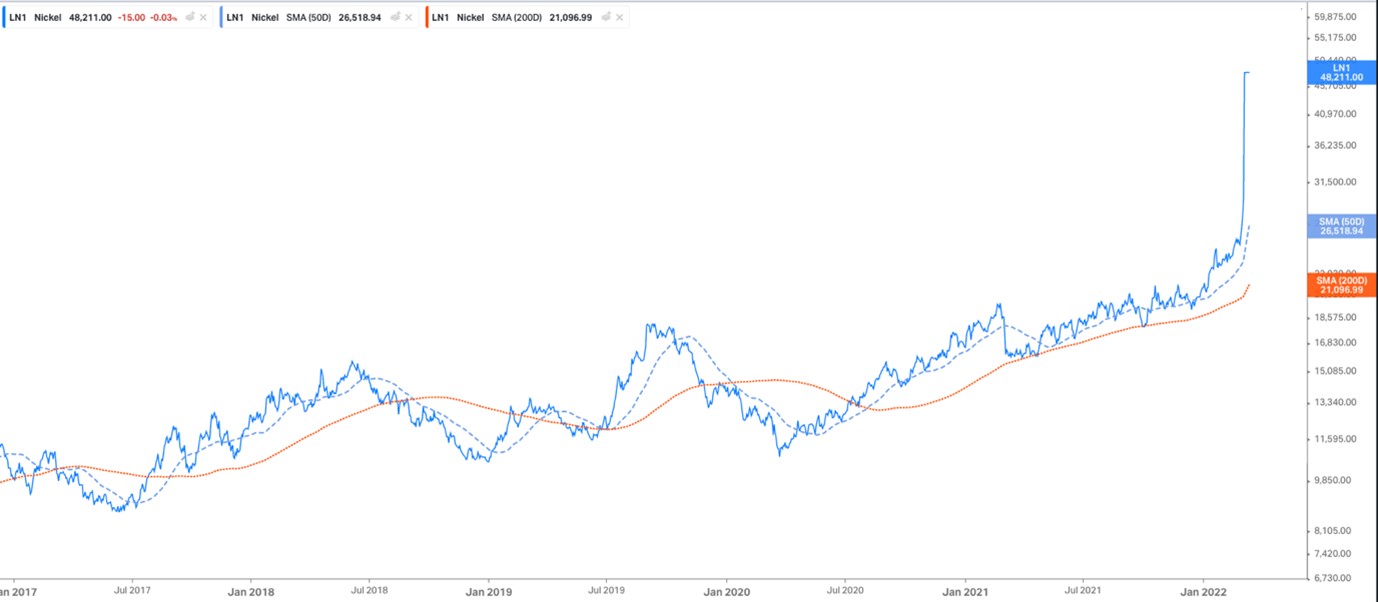

Amidst the chaos in commodities markets, nickel prices surged by 250% in an epic rise.

The London Metal Exchange (LME) has said it will resume nickel trading tomorrow, having called a halt last week after the metal’s price surged to $100,000 a ton in a massive, short squeeze. The LME will also bring in new rules setting daily upper and lower price limits for contracts for nickel and other base metals. The exchange was forced to suspend trading last Tuesday and cancel trades after Chinese tycoon Xiang Guangda’s company Tsingshan Holding Group bought significant amounts of nickel to cover short positions. Despite the metal’s rising price, the world’s largest nickel producer, kept buying, driving the price even higher. Last Tuesday, nickel touched a price double of its Monday closing price of $48,078 – already affected by concerns about a supply shock from Russian sanctions.

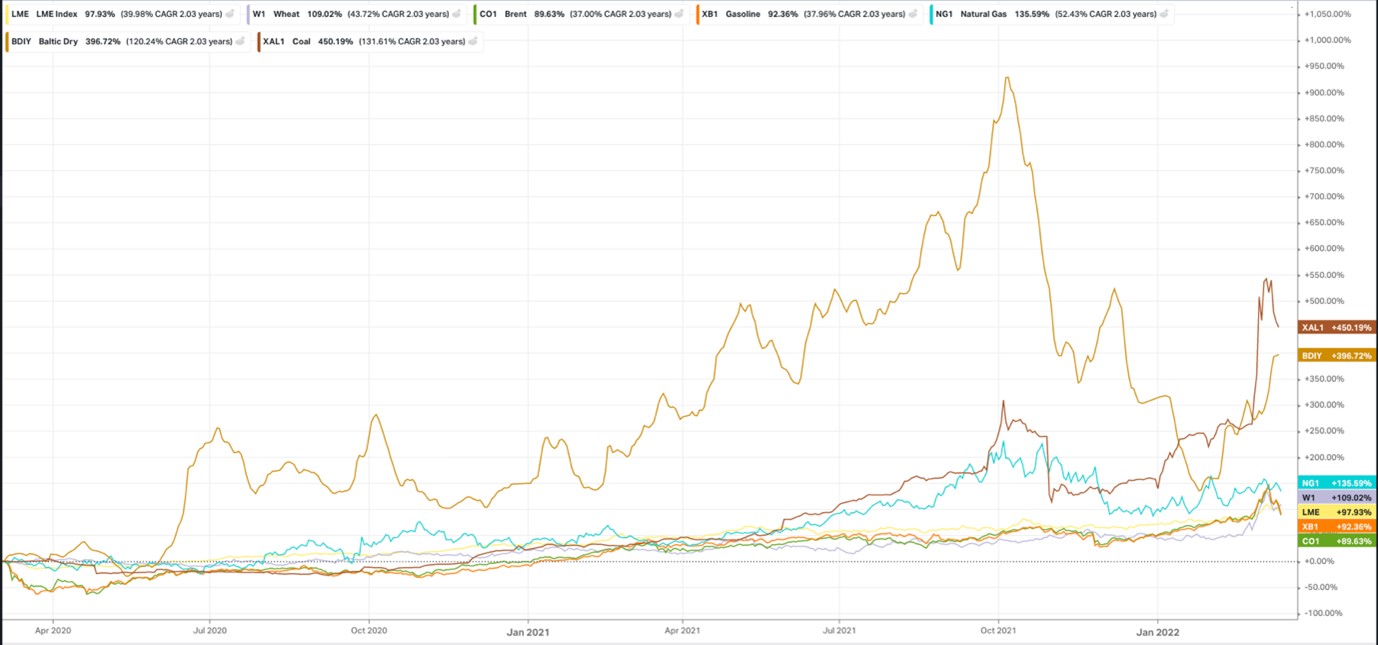

We are seeing prices of commodities violently surge and then retrace whipsawing retail traders out of their positions if they lose discipline and chase the markets. However, listening to producers who find the metal in the ground, they are now re-rating their forward guidance based on prices for base metals like nickel staying elevated for longer. This then becomes a problem for the end user of the base metal or whichever commodity is in question. Ideally the price would be passed on to the customer, but that has its limits too.

Market participants, including the European Steel Association, have commented on the impacts on the manufacturing sector. Furthermore, lithium iron phosphate (LFP) batteries, which do not contain nickel, have been less expensive. Thus, they are more likely to be used in some EVs than nickel containing NCM (nickel, cobalt, manganese) and NCA (nickel, cobalt, aluminium) storage solutions. Elon Musk recently Tweeted that Tesla and SpaceX were seeing significant inflation and if you go on to the Tesla configurator the prices have already increased as the manufacturer passes on the increase in raw materials. The largest price increases being on the Model 3 Performance, SUV’s and Model S. It is unlikely that the Tesla’s will be switching to cells with less nickel, so the only hope is for base metals to come back to the mean.

{kind=link}