Copper prices have been range-bound in recent months due in part to concerns over China’s property market and global auto manufacturing. COVID-19 is still causing disruptions as we approach 2022, and China is still not bailing out their failing property developers, so there is a likelihood that demand is lower into the H1 of 2022. As global growth picks up and bottlenecks in the supply chain begin easing, copper prices are likely to remain supported by the small supply deficit. If there is a sudden boost to demand, we are likely to see a big move in the base metals as the supply is generally tight. A key concern is the level of inventories at the London Metal Exchange, especially for copper and zinc. As a result of production cuts post the Great Financial Crisis in 2007-2009, producers had reduced CAPEX, so any supply overhangs were generally limited, to begin with. With COVID-19 resulting in a mining disruption but also demand destruction, there had not been a major push to find new resources. This is changing as commodity prices stay relatively high and vaccinations ease the health pressures and disruptions.

As a result of COP26, developed nations are under pressure to decarbonise, and China will play a key role in reducing global carbon emissions. In preparation for the Winter Olympics, China has proven that it can achieve blue skies over Shanghai under international scrutiny. In addition, they will need to upgrade their electricity infrastructure and electrify more and although the Chinese authorities are likely to utilise their coal power stations, there is a relatively large adoption of Electric Vehicles.

The London Metal Exchange copper inventories remain low but by 2023, a possible surplus could emerge as rising mine supply picks up. The commercial reporters on the CTFC show that the producers are adding to their overall short positioning, which is a sign that they want to lock in these current prices. An oversupply would obviously result in lower prices and shorting the physical is a good hedge.

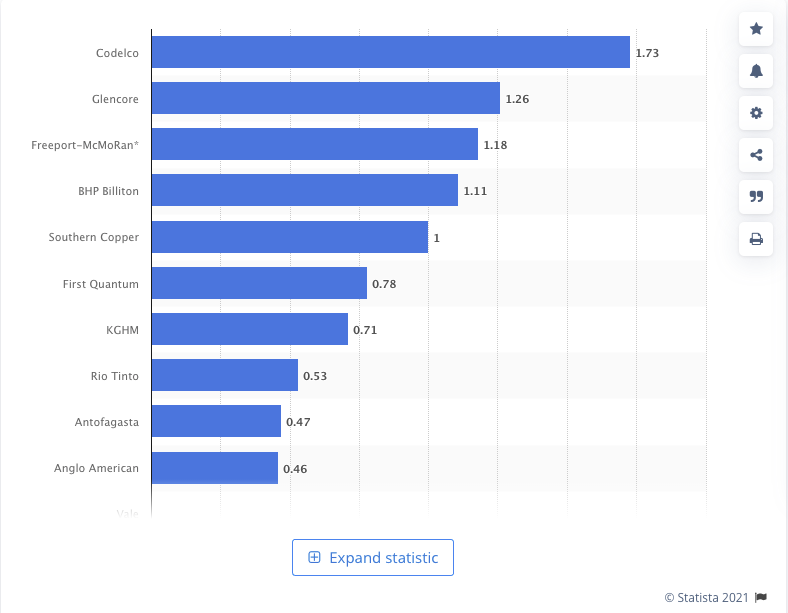

Copper prices also dropped last week as the dollar rally slammed the Chilean peso. On Sunday, Jose Antonio Kast garnered 27.9% of the vote, followed by left-wing candidate Gabriel Boric with 25.8%, and the election will now go to a runoff on December 19, 2021. Political unrest a couple of years ago has built up quite a lot of uncertainty and the hope is that come 2022, the new Chilean President will be able to restore some order.

{kind=link}