Roll on 14 months and we learned from the International Energy Agency (IEA) that global oil demand may rebound to levels seen before the pandemic in another year’s time, signalling a speedier recovery than its previous estimates. Whilst in today’s meeting from OPEC+, they agreed to increase output to July due to what they saw as a tight oil market. OPEC+ will meet again on 1st of July and by then will have a better sense of how much oil Iran will add to the global supply. “India’s Covid crisis is a reminder that the outlook for oil demand is mired in uncertainty,” the IEA said in its April 2021 Oil Market Report (OMR).

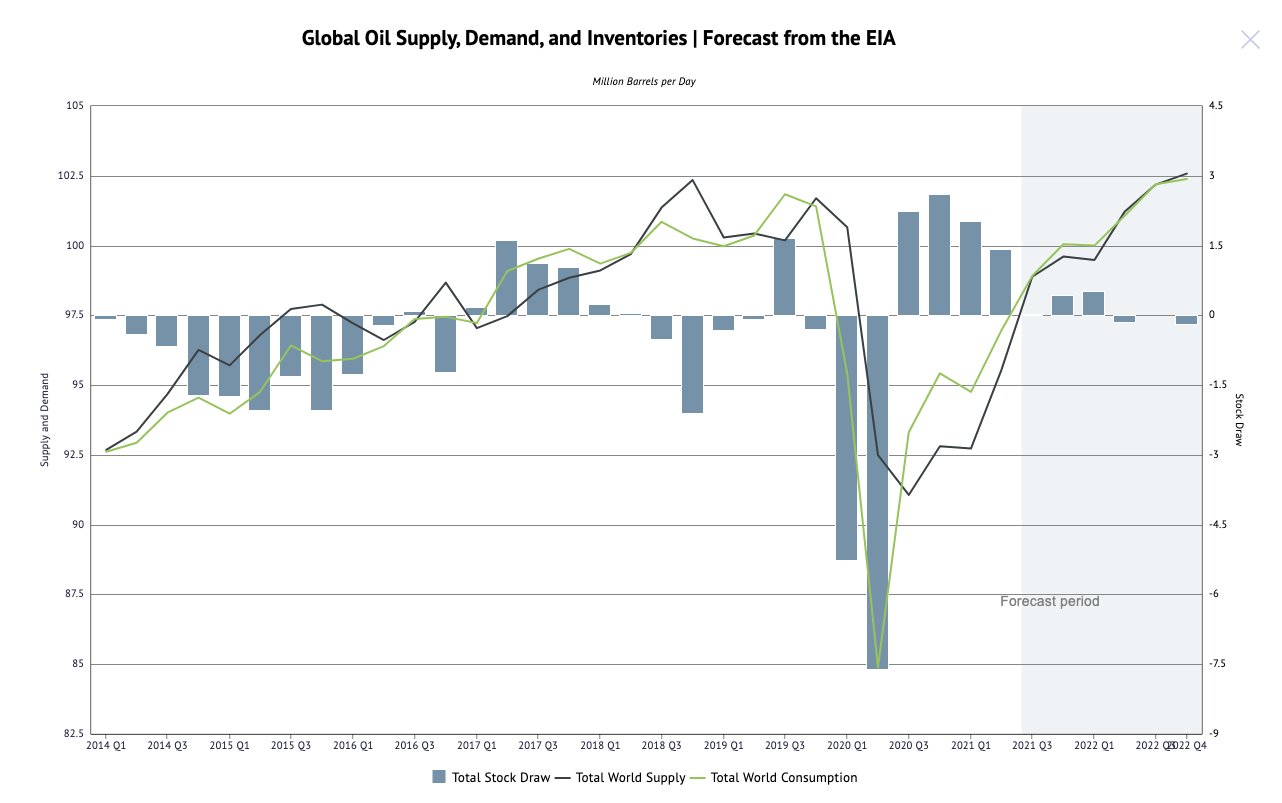

It revised demand lower in Europe and OECD Americas by 320,000 b/d and 515,000 b/d respectively in the first quarter, and cut its forecast for demand in India in the second quarter by 630,000 b/d. But it expects demand to jump to 99.6mn b/d in the last three months of 2021, compared with 93.1mn b/d in the first quarter, as vaccination rates rise and mobility restrictions ease.

The IEA said that based on the current OPEC+ agreement, it sees global oil production growing by 3.8mn b/d for the rest of the year.

In the latest IEA report, it said “After nearly a year of robust supply restraint from OPEC+, bloated world oil inventories that built up during last year’s Covid-19 demand shock have returned to more normal levels. While the market looks oversupplied in May, stock draws are set to resume from June, even with global oil supply on the rise.”

In his remarks at the 30th Joint Ministerial Monitoring Committee (JMMC), which was a videoconference affair due to travel restrictions, OPEC secretary general Barkindo, noted that projections continue to indicate a positive trajectory for economic and oil demand growth, especially in the second half of 2021. The President and Angolan Minister of Mineral Resources & Petroleum, Dr. Diamantino Azevedo, pointed out that the global vaccination rollout is creating optimism for global economic growth and world oil demand.

Earlier the IEA Executive Director, Fatih Birol said: “One thing is clear: In the absence of changing the policies, with the strong growth coming from the U.S., China, Europe, we will see a widening gap” between supply and demand. This, “in turn would put further upward pressure on the prices.”

{kind=link}