There was quite a lot of data out today from the US session which has helped keep the US dollar index above $95.50 but unable to breach the resistance level of $95.80.

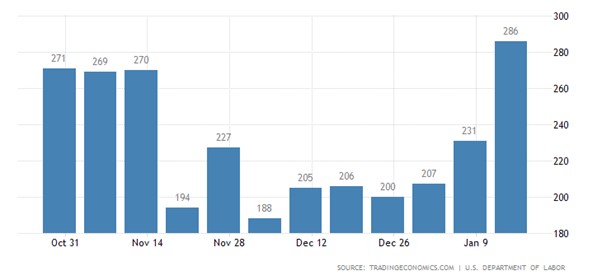

Initial jobless claims last week were much higher than expected at 286K, an increase of 55K over the previous week’s revised higher figure. The trend is going in the wrong direction as it has reached a 3-month high. A spike in COVID-19 cases spurred by the Omicron variant disrupted business activity as employers struggled to retain workers amid record levels of employee resignations. The US Jobless Claims 4-week average came in higher at 231.00K

US Philly Fed Business Index for January came in higher than expected at 23.2 and above the previous reading of 15.4. Orders were up but so were prices paid adding to the inflationary story. Employment was down.

According to the National Association of Realtors (NAR), existing-home sales in the United States fell 4.6% in December from the previous month, reaching a seasonally adjusted annual rate of 6.18 million, below market expectations.

On an annual basis, the figure rose by an astonishing 8.5%, its highest level since 2006. For all housing types, the median existing-home price increased by 15.8% to $358,000 from December 2020

US EIA Weekly Crude stocks were higher by 0.515Million barrels. Versus an expected draw of -0.938Million barrels. Gasoline was also a build whereas Distillates which is diesel and commercial fuels was a draw of -1.431Million barrels.

{kind=link}