As the country prepares for its general election, Prime Minister Fumio Kishida dissolved the upper house of the country’s parliament. “I want to use the election to tell the people what we’re trying to do and what we’re aiming for,” Kishida told reporters.

In the overnight session, Japan’s Ministry of Economy, Trade, and Industry (METI) announced the country’s industrial production index for August was 94.6 points, 3.6% lower than last month. The industrial output rose by 8.8% year over year. The shipment index increased by 7.2% year over year, while inventories dropped by 3.7%. Inventory ratios declined by 10% when compared with last year’s reading.

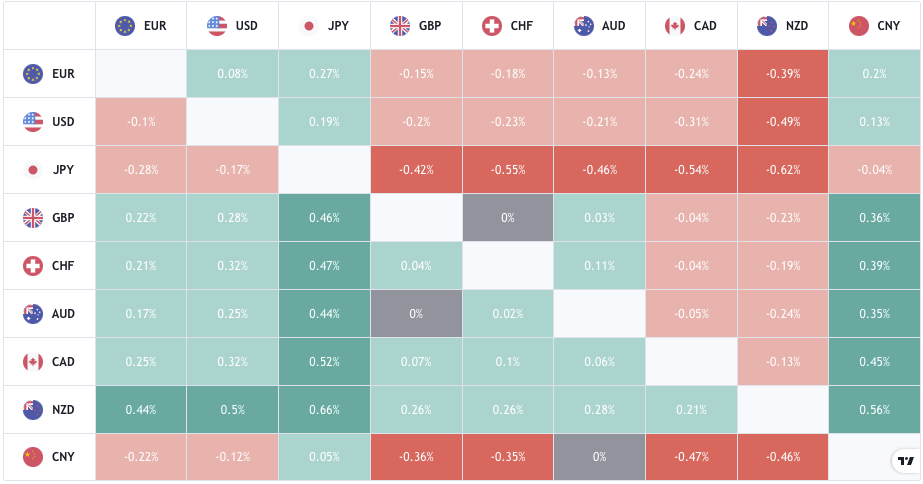

The yen continues to depreciate against the US dollar and is removing liquidity from above multiple swing highs from the descending channel. A move above 114.50 and there will be a clear run up towards 118.00 and major resistance.

{kind=link}